Why Short-Term Volatility is Masking Tungsten’s Long-Term Strategic Importance

Every commodity has its moment.

Twenty years ago, it was iron ore.

A decade later, rare earths briefly captured the world’s attention before fading back into the background (although admittedly, it is again garnering attention). More recently, lithium became the poster child of the energy transition, attracting billions of dollars of investment before reality reminded investors that even great long-term stories can experience painful corrections.

Tungsten has never enjoyed that moment.

In fact, if you asked most investors to name the world’s most strategically important critical minerals, tungsten probably wouldn’t make the list. Most would mention lithium, copper, uranium or rare earths. Yet I’d argue that tungsten deserves to be in that conversation.

I’ve spent much of the last two decades advising mining companies, industrial consumers, and investors across a broad range of commodity markets. One thing I’ve learnt is that the best opportunities rarely appear when everyone is talking about them. More often, they emerge quietly, while the market is distracted by something else.

That is where I believe tungsten sits today.

This isn’t because I think tungsten prices are about to move sharply higher.

Nor do I believe we’re about to see an immediate supply crisis.

In fact, I think many investors are asking the wrong question entirely.

Most commentary today focuses on short-term price movements. Is APT trading higher? Are Chinese exports slowing? Has demand from the tooling industry weakened?

Those questions matter.

But they aren’t the questions that will define the tungsten market over the next decade.

The more pertinent question is this:

Can Western economies realistically build secure tungsten supply chains outside China?

Everything else follows from that.

A Critical Mineral Hiding in Plain Sight

Unlike lithium or rare earths, tungsten doesn’t owe its importance to political narratives or fashionable investment themes.

Its importance comes from physics.

Tungsten possesses the highest melting point of any pure metal, exceptional hardness, remarkable density, and outstanding resistance to wear. Those properties make it extraordinarily difficult to substitute in many industrial applications. Academic work from the University of Cambridge and the British Geological Survey highlights that tungsten’s unique physical properties and limited substitutes underpin its designation as a strategically important raw material.

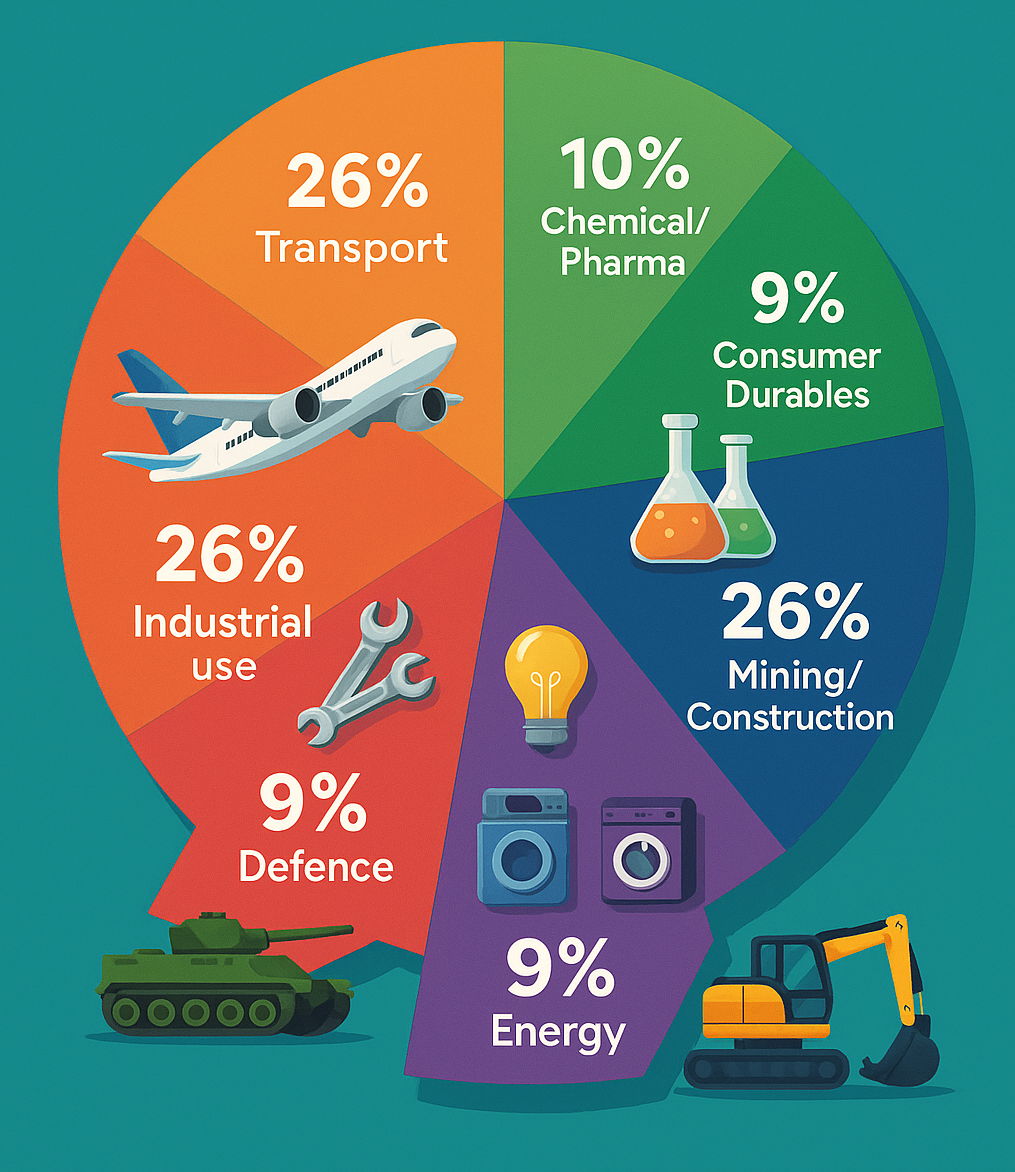

Tungsten applications are immense. We need tungsten, even if we don’t always realise it.

The cutting tools used to manufacture aircraft components.

The drill bits used in mining.

The wear parts used in heavy industry.

Machine tools.

Semiconductor manufacturing equipment.

Armour-piercing ammunition.

Rocket nozzles.

Oil and gas drilling.

Medical imaging.

In many of these applications, there simply isn’t another material that performs as well while remaining commercially viable.

That matters.

Because, unlike many commodities, tungsten isn’t dependent upon government subsidies. Nor is it built around one single industry. Instead, tungsten sits quietly inside almost every sector that advanced economies depend upon.

That makes it remarkably resilient.

The Market Is Looking in the Wrong Direction

One of the most common mistakes I see investors make is assuming that commodity prices tell the whole story.

They don’t.

Prices tell you what the market thinks today.

They don’t necessarily tell you what the market will need tomorrow.

Take tungsten.

Recent price volatility has encouraged many observers to conclude that the market remains comfortably supplied. Industrial activity has slowed in some regions, inventories have fluctuated, and buyers have periodically stepped back from the market.

On the surface, that seems reassuring.

Scratch a little deeper, and the picture becomes far less comfortable.

While prices have moved up and down, something much more significant has been happening.

Governments have started treating critical minerals as strategic assets rather than ordinary commodities. That represents a profound shift.

For decades, procurement decisions were driven almost entirely by price.

Today, security of supply has become equally important.

Defence departments are reassessing their dependence on overseas supply chains.

Manufacturers are asking where their material really comes from.

Governments are funding domestic processing capacity that would have been uneconomic only a few years ago.

Those decisions are not driven by today’s spot price.

They’re driven by tomorrow’s strategic risk.

China’s Dominance Is Bigger Than Most People Realise

When most people think about China’s position in the tungsten market, they think about mining.

That’s only part of the story.

China’s real strength isn’t simply that it produces most of the world’s tungsten. Its strength lies in the fact that it controls almost every stage of the value chain.

Mining.

Concentrates.

APT.

Tungsten oxide.

Metal powder.

Carbides.

Finished products.

That level of vertical integration is exceptionally difficult to replicate.

For years, this wasn’t viewed as a problem. Globalisation rewarded efficiency above almost everything else. Companies bought where prices were lowest, governments encouraged global trade, and very few people questioned whether concentrating so much supply in a single country posed a strategic risk.

That world no longer exists.

Today, supply security has become a boardroom discussion.

Governments are asking where critical materials originate. Defence departments are reviewing supply chains. Manufacturers are looking beyond cost and increasingly considering resilience.

This isn’t unique to tungsten. We’ve seen similar conversations around rare earths, gallium, germanium and antimony.

The difference is that tungsten has received far less public attention despite arguably being just as strategically important.

Why Building New Mines Isn’t Enough

Whenever governments announce plans to diversify critical mineral supply chains, the conversation almost always begins with mining.

That makes for good headlines.

It also oversimplifies the problem.

Bringing a new tungsten mine into production is challenging enough. Permitting, financing, construction, and commissioning can easily take the better part of a decade.

But mining is only the beginning.

Concentrates still need to be processed into ammonium paratungstate (APT), converted into oxides or powders, manufactured into carbides, and eventually transformed into finished industrial products.

Figure 1: Production of Metallic Tungsten and Tungsten Carbide from Natural Wolframite and Scheelite via Sulfide Chemistry

That downstream processing infrastructure has taken decades to build in China.

Replicating it elsewhere will require not only significant capital investment but also technical expertise, long-term customer relationships, and, perhaps most importantly, confidence that demand will remain strong enough to justify those investments.

This is one of the reasons I believe many investors underestimate how long supply chain diversification will actually take.

In short, opening a mine is challenging.

Rebuilding an entire industrial ecosystem is considerably harder.

Governments Are No Longer Thinking Like Commodity Buyers

One of the biggest changes I’ve noticed over the past five years is how governments talk about critical minerals.

Historically, the conversation focused on economic development.

Today, it increasingly revolves around national security.

That may sound like semantics, but it fundamentally changes how decisions are made.

National security doesn’t always seek the cheapest solution.

It seeks the most reliable one.

That distinction matters.

For decades, manufacturers optimised their supply chains for cost.

Governments are now encouraging them to optimise for resilience.

That inevitably changes investment decisions.

Projects that might previously have struggled to attract financing because they sat higher on the cost curve suddenly become strategically valuable.

Processing facilities that once appeared commercially marginal become national infrastructure.

Long-term offtake agreements become more important than short-term pricing.

We’re already seeing this play out across several critical mineral markets.

I believe tungsten will increasingly follow the same path.

The Market Is Still Focusing on Prices

Commodity markets have a habit of reducing complex industries to a single number.

Copper becomes today’s LME price.

Iron ore becomes the 62% benchmark.

Gold becomes the spot price.

Tungsten is no different.

Whenever prices soften, commentary quickly turns negative.

Whenever prices rally, optimism returns.

I think that misses the bigger picture.

Short-term price movements tell us something about today’s balance between buyers and sellers.

They tell us very little about the industry’s strategic direction.

For example, a period of weaker industrial demand may reduce tungsten prices for several quarters.

That doesn’t suddenly make China’s dominance disappear.

Nor does it eliminate the strategic need for diversified processing capacity.

Nor does it reduce defence requirements.

These structural issues continue evolving regardless of what prices happen to do over the next six months.

As investors, it’s important to separate cyclical noise from structural change.

The two rarely move together.

Why This Time Feels Different

The tungsten market has experienced several false dawns over the past twenty years.

Prices recovered.

Projects were financed.

Optimism returned.

Then markets softened and interest faded.

I’ve watched that cycle repeat often enough to understand why some investors remain sceptical.

This time, however, I think the drivers are fundamentally different.

Previous cycles were largely driven by industrial demand.

Today’s market is increasingly being shaped by industrial policy.

That’s a profound distinction.

Industrial demand fluctuates.

Government policy tends to persist.

Countries are spending billions to secure critical mineral supply chains.

Defence budgets are increasing.

Advanced manufacturing is being reshored.

Semiconductor capacity is expanding outside Asia.

These trends aren’t driven by the business cycle alone.

They’re driven by geopolitics.

That doesn’t mean tungsten prices can only move higher.

Commodity markets are rarely that simple.

What it does mean is that the strategic value of secure tungsten supply is likely to increase even during periods when prices temporarily weaken.

Looking Beyond Today’s Headlines

It’s easy to become distracted by the latest export restriction, quarterly production report, or price movement.

Those developments matter.

But they shouldn’t obscure the bigger picture.

For decades, tungsten was treated as another industrial raw material.

Today, it is increasingly being viewed through a strategic lens.

That shift has profound implications.

It changes how governments allocate capital.

It changes how manufacturers secure supply.

It changes how projects are financed.

And ultimately, I believe it will change how investors value companies operating across the tungsten value chain.

The transition won’t happen overnight.

Supply chains rarely evolve quickly.

But once strategic thinking replaces purely commercial thinking, markets often begin moving in a very different direction.

I believe tungsten is entering exactly that phase.

Investment Implications

One of the biggest mistakes investors make in commodity markets is assuming that every opportunity begins with rising prices.

In reality, the best investment opportunities often emerge long before prices fully reflect changing fundamentals.

Tungsten may be one of those markets.

For much of the past decade, the industry has suffered from underinvestment. Low prices discouraged exploration, delayed new mine development, and left much of the downstream processing industry concentrated in China. As a result, today’s market is entering a period where strategic demand is increasing faster than the industry’s ability to diversify supply.

That doesn’t necessarily mean tungsten prices will move in a straight line higher. Commodity markets rarely behave that way. Demand will continue to fluctuate with manufacturing activity, inventories will rise and fall, and prices will periodically overshoot in both directions.

What has changed, however, is the backdrop against which those cycles will play out.

Governments are increasingly prioritising security of supply over the lowest cost. Defence spending continues to rise across much of the Western world. Industrial policy is encouraging domestic manufacturing, while export controls have highlighted the risks associated with highly concentrated supply chains.

Taken together, these factors suggest that future investment decisions are likely to be influenced as much by geopolitics as by traditional commodity fundamentals.

For investors, this means looking beyond the tungsten price itself.

The more important questions are:

- Which companies are capable of supplying reliable material outside China?

- Where is new processing capacity likely to emerge?

- Which projects are genuinely financeable, rather than simply technically attractive?

- Which management teams understand that downstream integration may become just as valuable as mining itself?

These are the questions that I believe will separate the winners from the rest of the field over the next decade.

What I’m Watching

Rather than trying to predict where tungsten prices will be next quarter, I believe there are several structural indicators that deserve far closer attention.

1. Downstream processing capacity outside China

New mines attract headlines, but processing capacity is likely to determine how quickly supply chains diversify. Announcements relating to APT production, carbide manufacturing and downstream processing facilities may ultimately prove more significant than individual mine developments.

2. Government-backed financing

Critical mineral projects are increasingly attracting support from export credit agencies, development finance institutions, and strategic government programmes. Continued public-sector involvement would reinforce the view that tungsten is moving from being treated as a commodity to being regarded as strategic infrastructure.

3. Long-term offtake agreements

One of the strongest indicators of confidence in any commodity is the willingness of industrial consumers to commit to long-term supply agreements. These agreements provide financing certainty for producers while demonstrating that end-users are prioritising security of supply.

4. Defence procurement

The relationship between defence spending and critical minerals is becoming increasingly important. While defence demand alone will not transform the tungsten market, it provides a stable and strategically important source of long-term consumption.

5. China’s policy direction

China remains the dominant force in the tungsten industry and will continue to shape market dynamics for years to come. Export policies, environmental regulations, mine rationalisation and industrial strategy will remain among the most important variables influencing global supply.

Final Thoughts

For years, tungsten has quietly sat in the shadow of more fashionable commodities.

Lithium dominated the energy transition.

Rare earths became synonymous with geopolitical tension.

Uranium re-emerged as countries reconsidered nuclear power as a clean and reliable energy source.

Meanwhile, tungsten continued to underpin manufacturing, defence, and industrial production with relatively little attention outside specialist circles.

I don’t believe that will remain the case.

The conversation around tungsten is changing.

Not because the metal itself has changed, but because the world around it has.

Governments are beginning to recognise that resilient supply chains cannot be built overnight. Industrial consumers are increasingly looking beyond price when securing critical raw materials. Investors are gradually appreciating that strategic importance and market size are not always the same thing.

In my view, this transition is still in its nascence stage.

There will undoubtedly be periods of price weakness. There will be projects that disappoint and expectations that prove overly optimistic. Commodity markets have always been cyclical, and tungsten will be no exception.

But if the last few years have taught us anything, it is that the cheapest supply chain is not always the most secure.

Ultimately, I believe the tungsten story is no longer simply about mining.

It is about industrial resilience.

It is about national security.

And increasingly, it is about who controls the materials that underpin modern manufacturing.

That is why I believe tungsten deserves far more attention than it receives today.

This article originally appeared in Metal Intel newsletter on LinkedIn. Metal Intel is an independent publication developed by Core Consultants covering commodity markets, critical minerals, geopolitics, and long-term resource investing.

Each edition explores the structural forces shaping global resource markets—moving beyond daily headlines to examine what they mean for investors, mining companies, industrial consumers and policymakers.

Work With Me

My work falls into four areas:

Strategic Advisory Commodity market studies, commercial due diligence, market entry strategy and investment screening for mining companies, industrial groups and investors.

Executive Consulting Independent advice on critical minerals, supply chains, offtake strategy, project evaluation and commercial strategy.

Speaking & Expert Networks Conference presentations, board briefings, executive workshops and expert consultations on commodity markets and critical minerals.

Research The Metal Intel Strategic Brief series provides in-depth analysis of commodity markets and long-term industry trends.

If your organisation is evaluating a commodity, project, acquisition or investment opportunity, I’d be happy to discuss how I can help.

Coming Next: Metal Intel Strategic Brief No.1

This article has focused on the broader strategic themes shaping the tungsten market.

For readers interested in a deeper analysis, I will shortly be publishing the first Metal Intel Strategic Brief:

Global Tungsten Outlook 2026–2030

A comprehensive review of:

• Global mine supply and development pipeline

• China’s position across the tungsten value chain

• Processing capacity and downstream bottlenecks

• Demand outlook by end-use sector

• Defence and geopolitical considerations

• Pricing dynamics and market structure

• Strategic implications for industry and investors.

The Strategic Brief will be available as a complimentary download for Metal Intel readers.